NEW YORK – While the right wing demonizes public employee pension plans as expensive giveaways to greedy fat-cat workers, they are actually far more cost effective than the 401k-style defined contribution plans fashionable in the private sector.

A defined benefit plan, which New York City workers have under their contracts, guarantees an employee a certain amount of money per month after retirement. The amount is generally based on salary and the amount of time on the job.

As the name implies, a defined contribution plan, like a 401k, spells out how much money an employee contributes to their retirement income while on the job, an amount generally matched by the employer. However, after retirement, no set amount is guaranteed per month: this is determined based on the amount of money put aside while on the job. Additionally, the funds are invested in stocks or elsewhere, and the value of the retirement savings can rise or fall depending on the market.

The findings contradict the logic of a national trend, which has been towards defined contribution plans. According to the AFL-CIO blog, “Because pension funds invest large amounts of money in markets, it becomes easy for naysayers to persuade people that defined-pension benefits are somehow more costly and riskier than the individual-based 401k model.”

The imagined additional costs of defined benefit plans have played into what has been considered a right-wing drive to demonize public employees as living luxuriously off of public money while private sector workers suffer.

“Public employees are under attack in New York and across the country,” said John Lui, New York City’s comptroller, a Democrat, earlier this year. “While those who work in the private sector are understandably worried about their own retirement security, misplaced threats against firefighters, police officers, and school teachers only fuel a race to the bottom promoting insecurity for everyone.”

Liu was speaking at the kickoff of Retirement NYC, initiated by Liu’s office to study the actual costs of the public retirement system. The National Institute on Pension Security and Pension Trustee Advisors conducted the report, A Better Bang for New York City’s Buck, released Oct. 24, on behalf of Liu’s office.

“Scapegoating and inflammatory rhetoric cannot serve as a substitute for the real facts and sensible reform,” Liu continued.

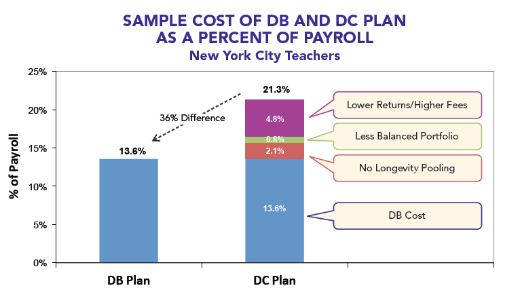

The city saves from 36 to 38 percent on the costs of the plan by providing defined benefit retirement packages, the report found.

Because the city itself manages the retirement funds, which are all pooled together, there is a much greater return on investment. The report notes this is “partly based on the lower fees that stem from economies of scale, but also because the assets are professionally – not individually – managed. The city plans’ enhanced investment returns save from 21 percent to 22 percent.”

The investments themselves also have a lower risk. “Because pensions pool the longevity risks of a large number of individuals and can determine and plan for mortality on an actuarial basis, New York City’s defined benefit plans save between 10 percent and 13 percent compared to a typical defined contribution plan.”

The pension assets themselves are also better invested in a defined contribution plan. “Because pension assets can be invested in a balanced and diversified portfolio at all times-as opposed to the life-cycle based investing of a 401k – the City’s defined benefit plans save from 4 percent to 5 percent,” according to the report.

As a portion of payroll, the savings are striking. For a teacher, the amount the city spends on a defined benefit plan is 13.6 percent of payroll. Were the city to switch teachers to a 401k plan, the cost, contrary to public perception, would actually rise to 21.3 percent of payroll – difference of 36 percent.

“These findings are consistent with our national study on the cost efficiencies embedded in pension plans,” said Diane Oakley, NIRS executive director, also in a press release.

“The analysis clearly indicates that the qualities inherent in [defined benefit] plans – particularly the superior investment returns and pooling of risks and assets – fuel their fiscal efficiency. The report provides important insight for policymakers, employers and employees, who are struggling to ensure adequate retirement income with the fewest dollars possible,” Oakley concluded.

Image: Cost as a percentage of payroll of pension plans by type of worker. Produced by the New York City Comptroller’s Office.

CONTRIBUTOR