Paul Krugman has long been skeptical of the success of the euro. The Nobel Prize winning Princeton economist, New York Times columnist and longtime Keynesian (stimulus) advocate to get the economy out of depression has repeatedly expressed his doubts on the viability of a single European currency in the face of political and fiscal disunity.

The European Union’s unwillingness/inability to spend money on expanding employment (in other words, fiscal policy) in managing European business cycles (recession and growth) gives them no tools with which to fight economic depression.

The EU set up a monetary union, but it needs a political union based on the empowerment of working people, not just bankers, to survive this crisis.

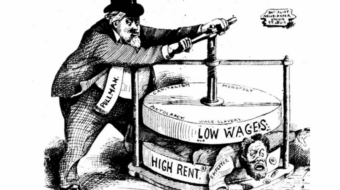

The main monetary tool for central banks to spur growth – lowering interest rates – is not possible once those rates approach zero. In addition, central banks without more democratic supervision, respond first to the ways in which economic cycles impact the financial system; they respond first to their most immediate clients – banks. Banks havea powerful and compelling interest to avoid anything which lowers the value of their loan and investment assets. This interest is no less powerful and compelling even if their lending and investment practices were foolish and reckless.

They will shamelessly beg for public bailouts when in trouble, but starve a whole nation before willingly inflating or taxing an additional penny of their wealth to help their fellow citizens. Those citizens, who were so kind to deposit their money in the bankers’ trust, or promise to pay back loans – even though many of the contract terms and resets were concealed in misleading language and assurances from lenders – are left ruined. Then they are lectured by the rich and their flunkies that poverty is really in their best interest — “the hungry dog hunts

harder.”

When the financial crisis of 2008 hit, the central bank in Europe and the leading EU countries – France and Germany – adopted a different approach than the U.S. Federal Reserve. The Obama stimulus package, and a fairly aggressive policy of easy credit by the Federal Reserve, was motivated by the mandate to reduce unemployment, not just keep inflation low. The stimulus and the easy money policy were not enough, says Krugman, to fix the depression, but they halted the downward trajectory of jobs and GDP.

European policy has been dominated by banker interests. There is no “reduce unemployment” mandate or obligation in the authority of the European Central Bank (ECB). There is no EU entity which can stimulate growth like a government, as well as absorb bad debt and distribute the losses across the EU. Thus ECB activity has focused on cutting EU member budgets under the now refuted theory that laying off more people will somehow instill markets with “confidence.”

Laying off more people in a depression has the opposite effect – it reduces GDP, reduces gross revenues for government, and debt gets worse, not better, after the cuts. This policy now has a global name: “austerity.”

Elections in Greece, France and Germany have punished the austerity policy.

In Greece, the political center has collapsed under the waves of layoffs and wage cuts forced upon Greek workers, leaving it currently without any governing coalition, and another election looming. France has rejected austerity with the election of Socialist François Hollande. Angela Merkel’s party in Germany suffered serious losses in parliament.

Krugman predicts the following.

1. Greek euro exit, very possibly next month, since previous commitments to pay down debt in exchange for loans were rejected at the polls. Political chaos is already stimulating a run on Greek banks as depositors try to move their money to safety.

2. Further huge withdrawals from vulnerable Spanish and Italian banks, as depositors there try to move their money to Germany, or other “safe” havens.

3. Spanish, Italian, Irish, Portuguese, Greek authorities (the PIIGS countries) may try to ban transfer deposits out of country and put limits on cash withdrawals and/or make huge draws on ECB credit to keep the banks from collapsing.

4. Germany either accepts huge indirect public claims on Italy and Spain (the largest troubled countries), or, the end of the euro.

This sequence of events seems highly likely. Krugman has been predicting it for over two years since the crisis began, and EU leaders have so far rejected the stimulus strategy which was the only hope of escaping this logic.

But it is a terrifying logic! And it is NOT the path to recovery. Disintegration in Europe is the path to aggravated conflict on every level, including peace and security. Recovery means investment, not cutbacks, in a depression. It means greater unity, not divisions, between EU nations and peoples. The working class must lead the way. But the way must be paved with internationalism. The fate of Greek workers will determine the fate of all EU workers. The election wave in Europe shows that working class and many democratic forces have awakened to the grave dangers that austerity forces have set in motion.

U.S. workers have a dramatic stake in the outcome. Another recession on top of the depression now threatens Europe. It will take the wind out of any hope we have of sustaining the anemic recovery we have here. The austerity forces here stopped the Obama recovery program two years ago. Krugman is pessimistic – but despite his brilliance as an economist – he has at times been politically numb. Let’s take that as a tonic. The lessons of Europe and the courageous reversal of austerity in the face of persistent threats from bankers and the rich give hope. When working people get moving – anything is possible!

CONTRIBUTOR

MOST POPULAR TODAY

AFL-CIO’s 30th Constitutional Convention kicked off in Minneapolis

AFL-CIO lays out most ambitious union organizing targets ever

Muslim woman’s car shot at in Dallas; police not investigating

Michigan nurses push back on Henry Ford Health union-busting tactics

The South African billionaires fomenting fascism and a global race war