AP—As Wall Street reels from the swift demise of Silicon Valley Bank—the biggest American bank failure since the 2008 financial meltdown—some social media users and conservative journalists are honing in on a single culprit: its socially aware, or “woke,” agenda.

But the Santa Clara-based institution’s professed commitment to diversity, equity, and inclusion, or DEI, wasn’t a driver of the bank’s collapse, say banking and financial experts. Its poor investment strategies and a customer base prone to make devastating bank runs were.

Here’s a closer look at the facts.

CLAIM: Silicon Valley Bank failed because it focused on “woke” corporate policies such as diversity, equity, and inclusion.

THE FACTS: The nation’s 16th largest bank collapsed because of poor investment and risk strategies that left the bank with insufficient cash to weather a mass withdrawal of assets from its largely tech sector customers, who have been particularly hard hit in the current economy, financial and banking experts explain.

There’s also no evidence to support claims that the bank’s stated commitment to supporting and investing in diversity and sustainability efforts played a role in its demise.

Social media posts as well as some op-ed posts in the wake of the collapse have nonetheless pointed critically to any number of diversity efforts at the bank, such as the launch of a month-long LGBTQ pride campaign or donations to Black Lives Matter and other racial justice causes.

Some even cited the bank’s 2022 Environmental, Social and Governance (ESG) report, which includes a commitment to provide at least $5 billion in loans, investments, and other financing for sustainability efforts by 2027.

“The WOKE agenda coming from SVB is in a large part to blame for their FAILURE,” declared a Twitter user in a post that had been liked or shared nearly 4,000 times as of Wednesday. “The insane left-wing agenda is BANKRUPTING our future. Go woke, GET BROKE!”

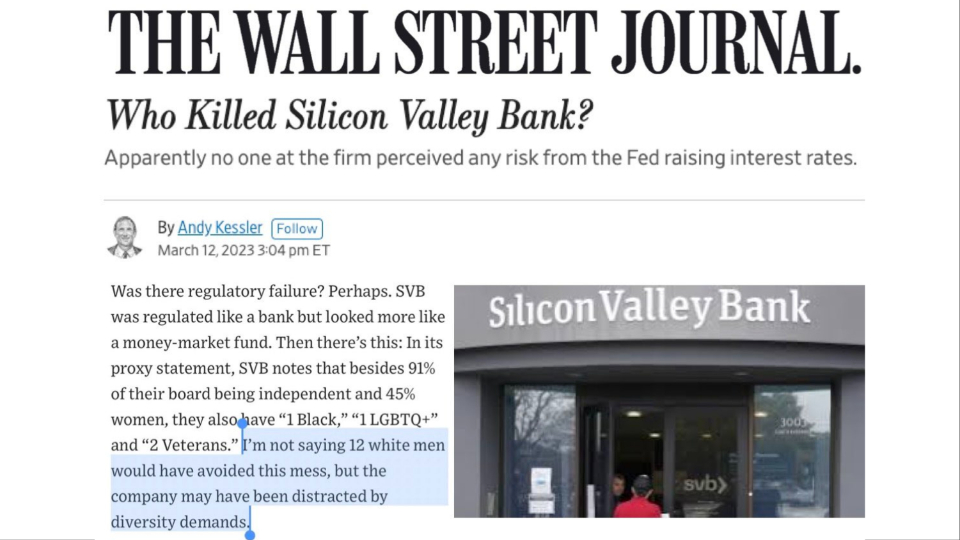

It wasn’t just the social media mob who resorted to such claims, though. Wall Street Journal columnist Andy Kessler wrote: “SVB notes that besides 91% of their board being independent and 45% women, they also have ‘1 Black,’ ‘1 LGBTQ+’ and ‘2 Veterans.’”

After listing off those whom he apparently thought were token add-ons, Kessler continued, “I’m not saying 12 white men would have avoided this mess, but the company may have been distracted by diversity demands.”

But SVB’s fall had all the hallmarks of a “classic run on the bank,” Peter Cohan, a professor of management practice at Babson College in Wellesley, Mass., said in an email. “A focus on DEI had nothing to do with the collapse of SVB.”

Rodney Ramcharan, a finance professor at the University of Southern California’s Marshall School of Business, agreed, dismissing the more than $70 million in tax deductible donations the bank reportedly made to BLM and other groups over the years as “trivial and irrelevant.”

Nothing in the bank’s publicly available financial disclosure reports suggests any damaging spending on diversity initiatives, he added. If there had been issues, they would be included in reports to regulatory agencies such as the Federal Reserve.

“The bank would have suffered loan losses—writing down bad loans made to ‘woke’ firms,” Ramcharan explained in an email. “So this is not a matter of opinion, but actual data. Instead, there are no unusual loan losses or loan loss provisioning.”

The bank’s $5 billion commitment to sustainability efforts represents a promise to make future loans and isn’t indicative of financial investments that led to the bank’s failure today, said William Chittenden, a professor at Texas State University’s McCoy College of Business Administration.

“If we were in 2027 and SVB had billions in defaulted ‘sustainability loans,’ then I would agree that the failure could be attributed to the types of loans they made,” he wrote in an email. “But to say the bank failed for loans they likely haven’t even made yet makes no sense to me.”

What is clear from financial disclosure documents is that the bank, which was founded in 1983, had not properly managed the risk on large investments it had made in recent years as it rapidly grew, experts agreed.

From 2019 to 2021, SVB purchased tens of billions of dollars in mortgage-backed securities, U.S. Treasury bonds, and other relatively conservative investments at low interest rates, explained Aaron Klein, a financial expert at the Brookings Institution, a D.C.-based think tank. But the bank didn’t hedge those bets with other investments.

As interest rates rose rapidly this past year, the value of those investments declined just as the bank’s customers were increasingly drawing down on their funds to make ends meet in a worsening economy, he and other experts said. The bank was forced to sell $21 billion of securities at a nearly $2 billion loss.

“Bottom line: The bank failed because of liquidity issues,” Chittenden wrote in an email. “The failure had nothing to do with the quality of any ‘woke’ bank loans.”

Another crucial factor in the bank’s demise was its client base, according to Klein.

The bank served mostly technology and venture capital-backed companies, including some of the industry’s best-known brands. But nearly all of them were considered uninsured depositors, meaning their accounts contained more than the $250,000 covered by the Federal Deposit Insurance Corporation in the event of a bank’s failure, he said.

“Uninsured depositors are more likely to run, making the bank inherently less stable,” Klein wrote.

Ironically, despite all the claims of being a “woke bank,” SVB wasn’t even all that diverse, at least at critical leadership positions, noted Peter Conti-Brown, a professor of financial regulation at the University of Pennsylvania’s Wharton School.

The bank’s executive team was all white and mostly male, and its board of directors had—as the Wall Street Journal reminded the world—just one Black member and one LGBTQ member.

Spokespersons for the bank didn’t respond to requests for comment, and the FDIC and other federal and state regulatory agencies declined to comment.

“There’s nothing unusual in SVB’s focus on diversifying away from such homogeneity—banks and businesses of all shapes and sizes have done the same,” Conti-Brown wrote in an email, referring to the company’s leadership team. “SVB failed because its bankers were bad at being bankers, something that no extra time away from meetings about diversity would have fixed.”

CONTRIBUTOR