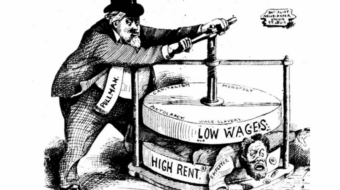

If you listened to the recent testimony of Wall Street executives before the bipartisan commission looking into the financial crisis, you would think that they were mere innocent spectators to it all.

That takes a lot of …. You can fill in the blank.

Did the Masters of the Universe really think that housing prices could only go in one direction – up, that investor risk was a non-issue in their financial games, that economic turbulence was a thing of the past?

I know that many economic theorists peddled these notions in recent years, actually going back to the late 1970s. Federal Reserve Bank governor (now chairman) and former Princeton economics professor Ben Bernanke, for example, asserted in a speech in 2004:

“One of the most striking features of the economic landscape over the past 20 years or so has been a substantial decline in macroeconomic volatility. … Several writers on the topic have dubbed this remarkable decline in the variability of both output and inflation ‘The Great Moderation.'”

Then the supposedly erudite Bernanke went on to say:

“The increased depth and sophistication of financial markets, deregulation in many industries, the shift away from manufacturing toward services, and increased openness to trade and international capital flows are other examples of structural changes that may have increased macroeconomic flexibility and stability.” (my italics)

Such was the conventional wisdom of the economics profession and too many politicians, Republican and Democratic alike.

Still, I doubt that the “titans” of finance, who manipulate money and markets 24/7, embraced this “wisdom” entirely. Unlike university professors, they have to pay attention to what is happening in the real world. The bottom line is what guides their behavior, not high-sounding generalizations resting on unrealistic assumptions (free, efficient and self-correcting markets, for example).

So assuming that I am right, that financial executives themselves, unlike the free-market theorists, kept at least one eye on the real world, and further assuming that they aren’t just plain stupid, why did they continue to invest in bundles of subprime mortgages of deteriorating quality in terms of return and risk? Why didn’t they reconsider their investment bets in a ballooning and increasingly unsustainable housing market in which prices got so out of whack with actual value?

The short answer is that financial firms operate in a very competitive capitalist market in which there are internal and external compulsions to accumulate higher and higher profits in the short term. (That get-rich-quick compulsion was aptly summarized by economist John Maynard Keynes, who famously said: “In the long run, we are all dead.”)

The longer, and more revealing, answer is that a few giant firms dominate the financial industry, and with size comes competitive advantage – resources and connections, an ability to make deals on both sides of the market (when it is going up and when it is coming down) – and an assumption (backed by earlier precedent) that the government will bail out these same firms when trouble arises. As a result these “too big to fail” financial institutions are both unafraid to ride the speculative wave as long as it lasts and also nimble enough to pull themselves safely out of turbulent waters when the wave breaks – so they think.

In other words, the financial giants are positioned to win no matter what the outcome. There is no better example of this phenomenon than Goldman Sachs. As the Security and Exchange Commission complaint alleges and as Michaels Lewis’s new book “The Big Short” discusses in some detail, Goldman Sachs (and probably other financial giants) played all sides of the market and, not surprisingly, broke laws while doing it and suckered the government into cleaning up its bad bets with taxpayer dollars.

To be more specific, Goldman was drowning in mounting piles of worthless securities and was effectively insolvent (more liabilities than assets), as many of its bets on subprime mortgages went sour (not all of its bets though, because it shrewdly and apparently illegally bet that the housing bubble would burst – “shorting” the market – which brought billions into its coffers).

In the meantime, Goldman executives, arguing (correctly) that financial markets occupy a strategic position in the overall economy and relying on their web of connections with the White House, Congress and federal agencies, rushed to Washington and demanded ransom money and a Wall Street fix to the market meltdown. Washington quickly obliged.

In hindsight, President Obama and congressional Democrats, for whatever reason, and there is more than one, missed an opportunity to insist that the biggest financial institutions be placed under public democratic control or, more modestly, broken up and scaled down in size. Public opinion, shaken by the enormity of the crisis and seething with anger towards Wall Street, could have been mobilized to support such far-reaching measures.

Now the moment is less opportune. Nevertheless, anti-bank anger continues and some form of financial regulatory reform is going to become the law of the land. The question is: will the new law have teeth?

Will it break up “too big to fail” banks?

Will it bring the shadow banking system (hedge funds, private equity firms, etc.) and derivatives (financial instruments that bet on the future price of housing mortgages, interest rates, currencies, etc.) under tight control?

Will it establish a consumer protection agency with real power to rein in credit card companies and the like?

Will it increase leverage requirements (money on hand at financial institutions to cover outstanding bets on financial instruments, such as stocks, bonds, futures, swaps, options, etc.)?

Will it guarantee that regulators will be tough on and independent of financial institutions?

Will it provide for public oversight of the regulators and the Federal Reserve Bank?

Will it prohibit banks from selling derivatives and other exotic financial instruments?

Will it contain a tax on financial transactions?

All this will be decided soon. Much will depend on the bargaining posture of the president and the mobilization of the American people for real regulatory reform. So far the labor movement and its leadership are setting the pace. The rest of us need to get on board.

CONTRIBUTOR