The U.S. Census Bureau calculates that nearly twice as many older Americans qualify as poor than had been previously thought. At the same time, net worth disparity between younger and older is at an all-time high, according to a Pew Center Report.

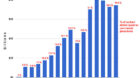

The Nov. 7 Pew Center report, conducted by Richard Fry, D’Vera Cohn, Gretchen Livingston and Paul Taylor brought to light a shocking gap: The median net worth, in 2010 dollars, for households headed by someone 65 years of age or older was $170,494 in 2009, 42 percent more than in 1984, when the median was $120,457, but still a pretty paltry figure.

But the median net worth for households headed by a person under 35 was, in 2009, only $3,662. Worse still, the 2009 figure represents a 68 percent decrease from 1984, when young households were on average worth $11,521.

Net worth is defined simply as assets minus debt.

And by definition, the median net worth is the middle value. There are an equal number of incomes above and below it. It is not skewed by extremely high or low incomes.

“As a result of these divergent trends,” notes the report’s introduction, “in 2009 the typical household headed by someone in the older age group had 47 times as much net wealth as the typical household headed by someone in the younger age group.” The 1984 ratio was only ten-to-one.

For young people, adulthood has been pushed back, meaning they enter the labor market later than their forebears and marry later. This, says the report, is part of the reason those under 35 have less wealth. Further, “Today’s young adults also start out in life more burdened by college loans than their same-aged peers were in past decades, as documented in a recent Pew Research report.”

But while recent events added to the inequality, the trends actually began appearing decades earlier. By another marker, income, older Americans are only treading water, while younger Americans are getting poorer. Those over 65 have seen their income rise by 109 percent. Those younger than 35 saw their incomes rise by only 27 percent. On average, Americans saw their incomes increase by 45 percent overall.

There is an added amount of inequality for African Americans and other people of color, as well as young mothers. “[T]oday’s young adults are more likely to be minorities and more likely to be single parents,” says the report. “These characteristics have been linked with lower economic well-being.”

Another reason for the discrepancy is a growth in inequality in home equity. However, said the report’s authors, “Trends over the same period in other key measures of economic well-being – including annual income, poverty, homeownership and home equity – all follow a similar pattern of older adult households making larger gains, compared with households headed by their same-aged counterparts in earlier decades.”

The trend was exacerbated by the housing market collapse, the Great Recession “and the ensuing jobless recovery.”

Housing played a major role: “If it had not been for home equity, the median net worth of older American households in 2009 would have been 33 percent lower than that of older households in 1984, instead of 42 percent higher.” Put another way, if home values had not risen as much as they had over the past few decades, older Americans would have also lost net worth, but at a slower rate than younger Americans.

Adele Stan at the AFL-CIO Now Blog cites the new U.S. Census Bureau model for calculating the nation’s poverty rate. The new data suggest that 16 percent of those 65 and older are poor. Under the old formula, which failed to accurately reflect housing and medical costs, the poverty rate for older Americans stood at 9 percent.

Kathleen S. Short, a U.S. Census Bureau economist, is quoted in the Los Angeles Times as saying that medical costs are pushing low-income seniors living on fixed incomes over the brink.

Photo: Meropi Peponides, 27, left, and John Smith, 31, of Brooklyn, N.Y., at the Occupy Wall Street protest Oct. 7, Zuccotti Park in Manhattan. Peponides is a graduate student who expects to have about $50,000 in loans when she graduates. Smith already has a master’s degree and about $45,000 in student loans, but can only find part time work. (Eileen Connelly/AP)

CONTRIBUTOR