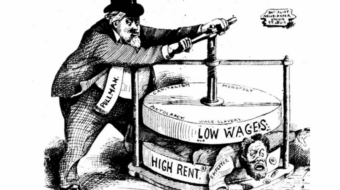

Goldman Sachs and J.P. Morgan Chase are back to the “old normal.” Profits are soaring – $3.2 billion and $3.6 billion respectively in the third quarter. Bonuses of $23 billion (yes, I got it right – 23,000,000,000 bucks) are in the pipeline for their managers and traders. Their field of competitors has thinned. And these leeches have morphed from “too big to fail” to “much too big” to fail.

In the meantime, the rest of us are fast-forwarding to the “new normal.” Let me explain.

A year ago the old model of capitalist accumulation (profit making) and right-wing political governance, resting on the rise of finance, mountains of debt, record levels of inequality, unsustainable global economic imbalances, and successive bubbles in real and fictitious assets came crashing down – not with a whimper, but with a bang that triggered an economic tsunami.

The U.S economy imploded, throwing people out of their jobs and homes, closing family farms, evaporating pension funds and savings, shuttering more plants and factories, and devastating cities and towns. Much the same occurred elsewhere in the world.

A complete collapse of the economy was dodged, but the crisis was the worst since the Great Depression and isn’t yet over. Unemployment levels, for example, are still rising. Reliable forecasts have joblessness climbing to nearly 11 percent officially in the United States.

Moreover, the prospects for a quick and robust recovery seem dim. Some economists, including mainstream thinkers, argue that economic stagnation is just as likely as a vigorous recovery.

In their view, the economy could operate at sub-normal levels in terms of growth, capacity utilization, employment, and income for an extended period of time. Or to put it differently, the tendencies toward stagnation are stronger than the tendencies toward full recovery.

Interestingly, this insight isn’t new:

“It is an outstanding characteristic of the economic system in which we live that … it seems capable of remaining in a chronic condition of sub-normal activity for a considerable period without any marked tendency either towards recovery or towards complete collapse.”

The author is British economist John Maynard Keynes, the quote is from his masterpiece, “The General Theory of Employment, Interest, and Money”, and the year is 1936. Keynes’ insight, however, fell out of favor among traditional economists with the resumption of vigorous growth in the core capitalist countries following WW II.

Ironically, it was Marxist economists, and especially Paul Sweezy and Harry Magdoff, who further theorized this dynamic of U.S. capitalism during this period.

But in the wake of the present economic crisis, Keynes’ notion of long-term sub-par economic performance is reentering the mainstream dialogue, but clothed with a new name – “the new normal.”

In the “new normal” universe, conditions for a fresh round of capital accumulation and economic growth exist on the supply side of the equation. Because of the depth and scale of the current downturn, inefficient plant, equipment, and businesses have been destroyed, a plentiful pool of unemployed wage labor is now available, the price of labor power (wages/salaries) is cheaper, interest rates are low, and economic power is further concentrated and centralized in the hands of fewer industrial, service and financial corporations.

But on the demand side of the equation, conditions for accumulation (profit making) are far less favorable. Demand (consumption and investment, domestic and global), and again because of the economic crisis (evaporation of wealth, layoffs, foreclosures, wage implosion, mountains of debt to be paid off, etc.) is insufficient relative to the productive capacity of the global economy. And there are many reasons to think that this will not change in the near or medium term.

Indeed, it is hard to see where the new dynamism to power economic growth, employment, research, and broadly shared income gains will come from other than a government financed and directed economic development project. Such a project should be sustainable, green, maximize worker and community input and decision making, and dynamic enough to give a growth impulse to the whole economy.

An obvious objection that will arise among friends, as well as foes, is that the federal deficit is out of control now and a project of this size goes way beyond the scope of government and would represent a massive intrusion into people’s lives.

The federal deficit is at record levels and there are dangers to be sure, but nothing as big as the danger (and costs) of long-term stagnation to the American people. Moreover, some of the financing could come from a reduction in the military budget and a shift of taxes to Wall Street and corporations.

As for government intrusion, federally directed development could encourage municipal and regional authorities to plan and organize major projects as well as channel investment dollars to small and medium sized businesses and worker/community cooperatives.

Whether a developmental project like this sees the light of day depends only in a small way on its feasibility and necessity. In a larger sense it rests on which of the competing sides (there are more than two on the political landscape) are able to frame the national conversation and win active popular majorities to its vision.

At this moment, political strength, moral authority, and public opinion tilts in the direction of the new administration and the broader movement that elected him, but not to the extent that it is able to win such radical economic reforms, assuming for the moment that everyone sees their necessity.

That task lies ahead.

Photo: A family’s residence in a tent city in East Providence, R.I. (Stephan Savoia/AP)

CONTRIBUTOR

MOST POPULAR TODAY

Michigan nurses push back on Henry Ford Health union-busting tactics

AFL-CIO’s 30th Constitutional Convention kicked off in Minneapolis

AFL-CIO lays out most ambitious union organizing targets ever

United Auto Workers announce choice for Michigan’s U.S. Senate seat: Abdul El-Sayed

Rebellion from below threatens overthrow of Bolivia’s new right-wing government