BLUE ISLAND, Ill.—For 33 years on Chicago’s South Side, Blue Island resident James Morgan helped bake Wonder Bread.

“When you’re in an industrial bakery, the work is difficult and demanding,” he says. And he did every job there was in that Wonder Bread plant, from slicing and wrapping to shoveling 50 pounds of dough at a time into the ovens.

It gave him a good middle-class life…but now he wonders if it’s going to be gone.

That’s because several years ago, Wonder Bread’s new owners, a group of private financiers, announced they were suspending the company’s contributions to the multi-employer pension fund Morgan and his fellow members of Bakery, Confectionery and Tobacco Workers and Grain Millers Local 1 had faithfully paid into.

They couldn’t afford it, the owners said. They promised to resume in a few months. They never did. Instead, they declared bankruptcy and closed the plant. And, with bankruptcy court permission, the financiers walked away from millions of dollars in pension obligations, while paying themselves nice fat checks, also with the court’s OK.

That left Morgan, a former Local 1 shop steward, and his co-workers and friends out in the financial cold. Don’t worry, he thought. He had his pension, plus a part-time job in a school. Or so it seemed.

But now that multi-employer pension fund Wonder Bread used to contribute to is in or headed for the “red zone” of such funds. It’s bleeding cash as the number of companies in it – especially after the 2008 Great Recession hit – crashed and the number of active workers did, too, victims of the joblessness that slump caused. The number of pension fund clients soared.

If that fund collapses, Morgan is left with zero.

“I stand to lose being independent and taking care of my family,” he told lawmakers on March 7. “I’m 67. Not too many people would hire a 60-some-year-old these days. I need my pension for food and medicine.”

That BCTGM fund is one of approximately 100 multiemployer pension plans projected to run out of money in the next 20 years, lawmakers learned at the hearing, the first of several on the problems plaguing those pension plans. They cover an estimated 1 million-1.5 million workers nationwide.

They’re union members because companies and unions jointly run those multi-employer pension plans. They’re Teamsters, BCTGM members, UFCW members, Steelworkers, Electrical Workers, Seafarers, Mine Workers, Machinists, and others. Especially Mine Workers.

And their multi-employer plans all suffer from the same financial ills: Too few workers and too few firms putting money in, and more and more retirees to care for.

The workers supposedly have a backstop: The federal Pension Benefit Guaranty Corp. (PBGC), set up to take over pensions for workers when companies walk away, buy their way out of contributions or avoid their obligations and dump their workers by declaring bankruptcy, as Wonder Bread did.

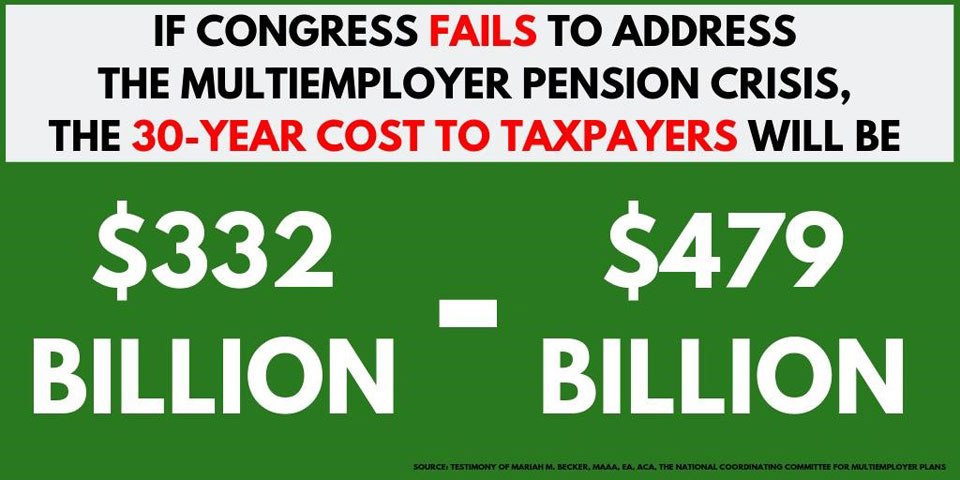

There are two problems with that scenario, though, other witnesses told the House Education and Labor subcommittee that deals with pension problems. One is PBGC’s average yearly payout per worker is $12,365. The average pension promised to each covered worker in a multi-employer plan: $27,300. “These aren’t golden parachutes,” one witness said.

And the other is the PBGC trust fund that handles the multi-employer plans suffers from the same financial ills its clients do: Fewer firms contributing, more bankruptcies and company walkaways, more aging workers, widows and dependents to cover. It’s $54 billion in the hole. It could run out of savings – leaving only company contributions – by 2025.

In short, unless Congress does something and quickly, Morgan says, one day he could wake up with a pension of zero. So could more than a million other workers, witnesses said.

That brought Morgan, along with members of the other unions facing multi-employer pension plan problems, to Congress to urge lawmakers to fix this mess, fast. It’s particularly acute for the Mine Workers, whose delegation of several dozen from Pennsylvania, Ohio and West Virginia spent three days in D.C. lobbying legislators.

The UMWA pension funds are in particular peril and they have a particular claim on the federal government: It set them up just over 70 years ago, funded by a per-ton tax on coal.

But there are now so few coal companies and so many “orphan” ex-miners and their widows to take care of – miners whose firms went out of business, leaving remaining companies to pick up the tab – that the UMWA funds could go broke within months. And in interviews before the hearing started, they’re even more worried than Morgan is. Though they didn’t say so, the prior GOP-run Congress ducked the issue.

“Our pension will be nothing because, in 2007, the stock market hurt us real bad,” followed by coal company bankruptcies, John Sismondi of United Mine Workers Local 2300 in Waynesburg, Pa., told People’s World. If the UMWA multi-employer plan went belly-up, “We’d have nothing. My wife is working now, but she has medical problems,” he adds.

“And try to find a job after you’re 65 years old,” says retiree Norman Sams of Local 762 in Uniontown, Pa. He’s worried not so much for himself, but for his widowed mother, Donnie, aged 87, surviving on her miner husband’s pension – which is a little over $400 monthly. If the UMWA plan tanks and the feds take over, that could be cut by $100 monthly or more.

So while the lawmakers took testimony and subcommittee Democrats, led by chair Frederica Wilson, D-Fla., promised to move quickly, the workers wait, worry and lobby. This was the second UMWA delegation to walk congressional halls in three weeks, discussing the multi-employer pensions issue.

Morgan and his allies got a positive reception for their problems from committee Democrats and all but one Republican. Indeed, Wilson and the top GOPer on the panel, Rep. Tim Walberg, R-Mich., together drafted legislation, HR397, to try to solve the problems.

“This is a promise for a secure retirement” that prompted workers “to put on hold” wage increases so more money could go to pensions, said Rep. David Norcross, D-N.J., a building trades leader in his state who is very familiar with multi-employer plans. “If we do nothing, the system crashes and takes everyone down with it.”

The lone dissenter was former full committee chair Rep. Virginia Foxx, R-N.C., who once questioned the need for unions at all. She called HR397 “a bailout.”

“The fundamental point about pensions is that they’re not charity,” responded Rep. Andy Levin, D-Mich., a former AFL-CIO deputy organizing director. “They (workers) put the money aside themselves and shame on us if we don’t provide it.”

“I was on the union bargaining committee” with Wonder Bread “and we’d negotiate wage increases of 35 cents or 40 cents an hour, and we’d take 12 or 13 cents of that and put it into the pensions,” Morgan said. Unless Congress acts, that money they earned is gone.

As a result, other witnesses noted, the pensioners, deprived of their income, would have to turn to public programs – food stamps, housing aid and the like – to stay alive.

To try to solve the problems, the bipartisan bill, the Rehabilitation for Multiemployer Pensions Act, would provide low-cost long-term repayable federal loans to funds in financial trouble, financed by 30-year government bonds. Estimates of the long-term costs of the bonds range from $34 billion-$100 billion. Estimates of the costs to government to aid the bereft pensioners are double that.

The funds could use the loans to both shore up their finances by making responsible investments while not cutting benefits for current retirees, a committee fact sheet says.

That would solve one big problem from the last time, several years ago, when Congress’ GOP majority tackled the multi-employer pension fund issue. Its law, passed in a rush at the end of the session, let financially troubled plans cut current benefits – in some cases by 40 percent or more – to try to guarantee future solvency, subject to a federal OK. Now they wouldn’t have to do that. Several unions and pro-union senators strongly opposed that legislation.

Labor appears to be united behind HR397. Backers include BCTGM, the Steelworkers, the Machinists, the Teamsters, the Food and Commercial Workers, the Electrical Workers and the Boilermakers, and the American Association of Retired Persons. HR397 will move, but not immediately, Morgan said afterwards. She wants those several more hearings first.

CONTRIBUTOR